Beware of all enterprises that require a new set of clothes.

Henry David Thoreau

Current Fed Interest Rate Stance Akin To Nonsense

Updated Jan 3, 2024

Just over a year ago, the Federal Reserve (Fed) embarked on its first rate hike in over a decade, promising similar moves throughout the following year. However, this pledge was empty, with no significant action until recently. Now, the Fed seems to be singing the same tune despite a track record that includes only two rate hikes in the past decade. It’s worth noting that the economic landscape was much more robust in 2006 and 2007 than it is today.

The recent statements from the Fed, particularly from Janet Yellen, underscore the Fed’s current stance and set the stage for another potential “oops, we were wrong again” moment. Yellen acknowledged the considerable uncertainty surrounding potential changes in economic policies and their impact on the economy.

Given the economic landscape has remained largely unchanged since the last rate hike, it begs the question: Is the economy truly more robust? The only discernible strength seems to lie in the illusion of economic recovery. If the economy were genuinely improving, a rising rate environment would be viewed positively. However, the reality is that this economic recovery is more illusion than substance, propped up by debt. Cutting the supply of hot money could lead to a market downturn. The real estate sector remains unstable, with many unable to afford homes. Raising rates in this scenario could spell disaster.

From our perspective, the Fed raised rates to create flexibility while attempting to convey reluctance to embrace negative rates. Striking a delicate balance, the Fed aims to keep the US dollar attractive globally, crucial for generating unlimited money as the world’s reserve currency. Without this status, the US might have faced challenges similar to Greece’s.

Fast forward to the present day, the Federal Reserve is expected to maintain the target range for the federal funds rate at a 22-year high of 5.25%-5.5%. This decision follows a 25bps hike in July as the central bank attempts better to assess the impact of high borrowing costs on inflation. However, the door remains open for another increase as early as November.

The US economy has proven surprisingly resilient due to robust consumer spending and a tight labour market. Although inflation remains above the 2% target, it is much lower than it was a year ago. The Fed’s preferred inflation gauge’s annual PCE rate increased to 3.3% in July from 3% in June. It compares with 6.4% in July 2022.

The Fed’s actions have real-world effects on how consumers and businesses can access credit to make necessary purchases and plan their finances. When interest rates change, consumers pay more for the capital required to make purchases, and businesses face higher costs tied to expanding their operations and funding payrolls.

In conclusion, the Fed’s current stance on interest rates seems to be more of a balancing act than a clear-cut strategy. While the central bank is trying to keep inflation in check and maintain the attractiveness of the US dollar, it’s also grappling with the potential fallout from higher borrowing costs. The question remains whether this approach will lead to a more robust economy or merely perpetuate the illusion of recovery.

The Dark Influence of the Federal Reserve

The role and influence of the Federal Reserve in the U.S. economy have often been a subject of much debate. Some critics argue that the Federal Reserve, despite its purported commitment to economic stability, perpetuates inequality and benefits the wealthy at the expense of the poor and the middle class.

One aspect of this argument is the claim that the Federal Reserve’s policies have led to the dollar’s devaluation. Indeed, since the Federal Reserve was established in 1913, the dollar has lost about 96% of its value. This depreciation in the dollar’s purchasing power is largely due to inflation, which some argue is a consequence of the Federal Reserve’s monetary policies.

The critics also suggest that the Federal Reserve fosters boom and bust cycles through its manipulation of interest rates. For instance, Alan Greenspan, the former Fed Chairman, was criticized for keeping interest rates too low for too long in the early 2000s, which some believe contributed to the housing bubble and subsequent financial crisis of 2008.

Another contentious issue is the Federal Reserve’s status as a quasi-public institution. While it is subject to congressional oversight, it operates independently of the government. Further, its regional Federal Reserve Banks are owned by private banks, leading to criticism that it is more beholden to banking interests than to the public. This was highlighted during the 2008 financial crisis when the Federal Reserve provided massive bailouts to banks while ordinary citizens suffered unemployment and foreclosures.

Finally, the Fed’s role in aiding financial institutions during crises has been criticized as contributing to the problem of moral hazard. If banks know they will be rescued, they have less incentive to avoid risky behavior. This was evidenced during the 2008 crisis when big banks were bailed out while small businesses and homeowners received less support.

Despite these criticisms, the Federal Reserve plays a critical role in maintaining the stability of the U.S. financial system. Its decisions significantly impact interest rates, inflation, and employment levels. However, the debate about its influence and the fairness of its actions continues, reflecting the complexities of managing a nation’s monetary policy.

Now, let’s delve into a historical perspective on the situation. We firmly believe that history serves as a guide for the astute, allowing them to master past patterns. In doing so, they can avoid repeating the mistakes of their forefathers and, instead, leverage the knowledge gained from history to profit in the face of the next disaster. Moreover, examining history provides insights into how we navigate through similar situations in real-time, offering valuable lessons and strategies for the present and future

Fed Previous Interest Rate Stance Indicates Hot Air.

Recall just over a year ago when the Fed initiated the first rate hike in over a decade, asserting that they would continue raising rates several times in 2016. However, this promise materialized into nothing until recently. The Fed is now repeating a similar narrative. It’s essential to highlight that the Fed has only raised rates twice over the last ten years. Notably, the economy was much more robust in 2006 and 2007 than it is today.

Yellen stated, “All the (Federal Open Market Committee) participants recognize considerable uncertainty about how economic policies may change and what effect they may have on the economy.”

Considering the unchanged economic landscape since the last rate hike, the question arises: Is the economy stronger? The only perceivable strength lies in the illusion of economic recovery. A rising rate environment would be viewed positively if the economy genuinely improved. However, the reality is that this economic recovery is more illusion than substance, propped up by debt. Cutting the supply of hot money could lead to a market downturn. The real estate sector remains unstable, with many unable to afford homes. Raising rates in this scenario could spell disaster.

Our perspective is that the Fed raised rates to create flexibility while attempting to convey reluctance to embrace negative rates. Striking a delicate balance, the Fed aims to keep the US dollar attractive globally, crucial for generating unlimited money as the world’s reserve currency. Without this status, the US might have faced challenges similar to Greece’s.

Current Fed Interest Rate Stance: Exploiting Global Resources

The Federal Reserve’s ability to generate money out of thin air allows the US to maintain its top position by essentially robbing the world, often at the expense of other nations. However, this dominance is precarious, with China looming as a potential usurper. On a purchasing power parity basis, China has already surpassed the US as the world’s largest economy. The world might one day realize the vulnerabilities of this system, but we won’t delve into that issue for now.

Our belief is that the Fed might ultimately have no alternative but to embrace negative rates, unless they want to trigger a market crash. Throughout history, the Fed has been notorious for artificially creating boom and bust cycles since the US departed from the Gold standard. While there are signs of a bubble-like phase in the stock market, it’s crucial to note that the majority of the population has not reaped significant benefits from the ongoing rally. Historical patterns indicate that the Fed typically intervenes to deflate the bubble once the masses fully embrace the market, continuing their complex role in what can be perceived as robbing the world to sustain domestic stability.

Markets only crash when the crowd is ecstatic.

Additionally, the masses are not euphoric; however, they are turning more bullish, which suggests, as we alluded to in this article Stock Market Bulls-Stock Market fools-Market Crash next or is this just an Illusion, that it would not surprise us if the markets experienced a decent correction next year. In the interim, we think the Fed’s current move is just a trick to make it appear to the world that our economy is healthy. Now, the Fed can lower rates twice before they move to zero, but it will force the rest of the world to lower their rates even more, effectively still making the US dollar the most attractive currency.

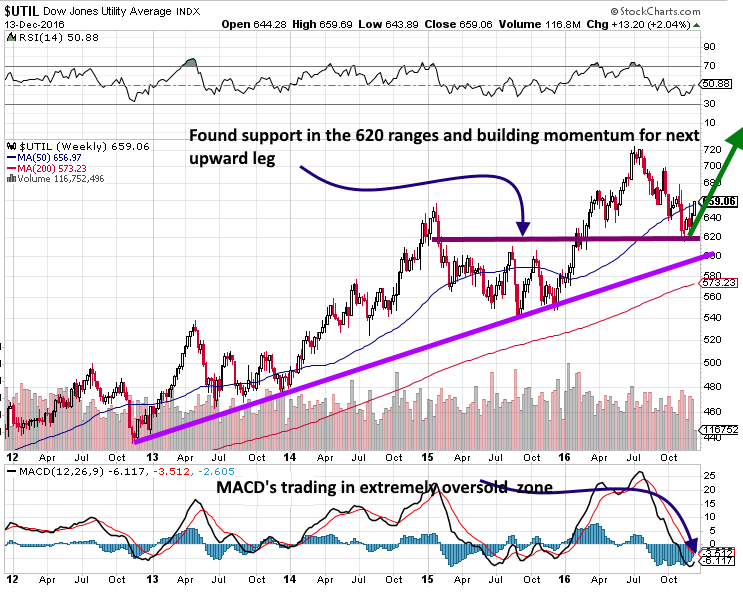

The bond market, which many have given up for dead, is looking for an excuse to rally sharply. We will look at this in more detail in a follow-up article. However, if you look at the long-term chart below, it is easy to spot that bonds have not crashed. They were pushed to extreme levels as individuals embraced bonds for years despite the miserable returns they offered due to the safety factor.

The Public Remains Apprehensive

The general public has maintained a sceptical stance toward this bull market, anticipating its imminent collapse for the past nine years. Following Trump’s victory, funds shifted from bonds to the stock market, indicating a simple rotation of money between markets. Currently, bonds are experiencing extreme overselling while the markets are trading near highly overbought levels. As the markets begin to retreat, funds will likely flow back into bonds, resulting in lower rates. This juncture will reveal whether the bond rally is merely a temporary rebound or if the bull market is poised for another surge.

This is a weekly chart containing five years’ worth of data (each bar represents one week’s worth of data); it is easy to spot that the Bond market is extremely oversold. Trump’s win has created a lot of enthusiasm, and many individuals sitting on the sidelines moved out of bonds and into the market. As the current upward move has been mighty, bonds could likely experience an equally strong counter-move.

Sentiment Shifts on the Horizon

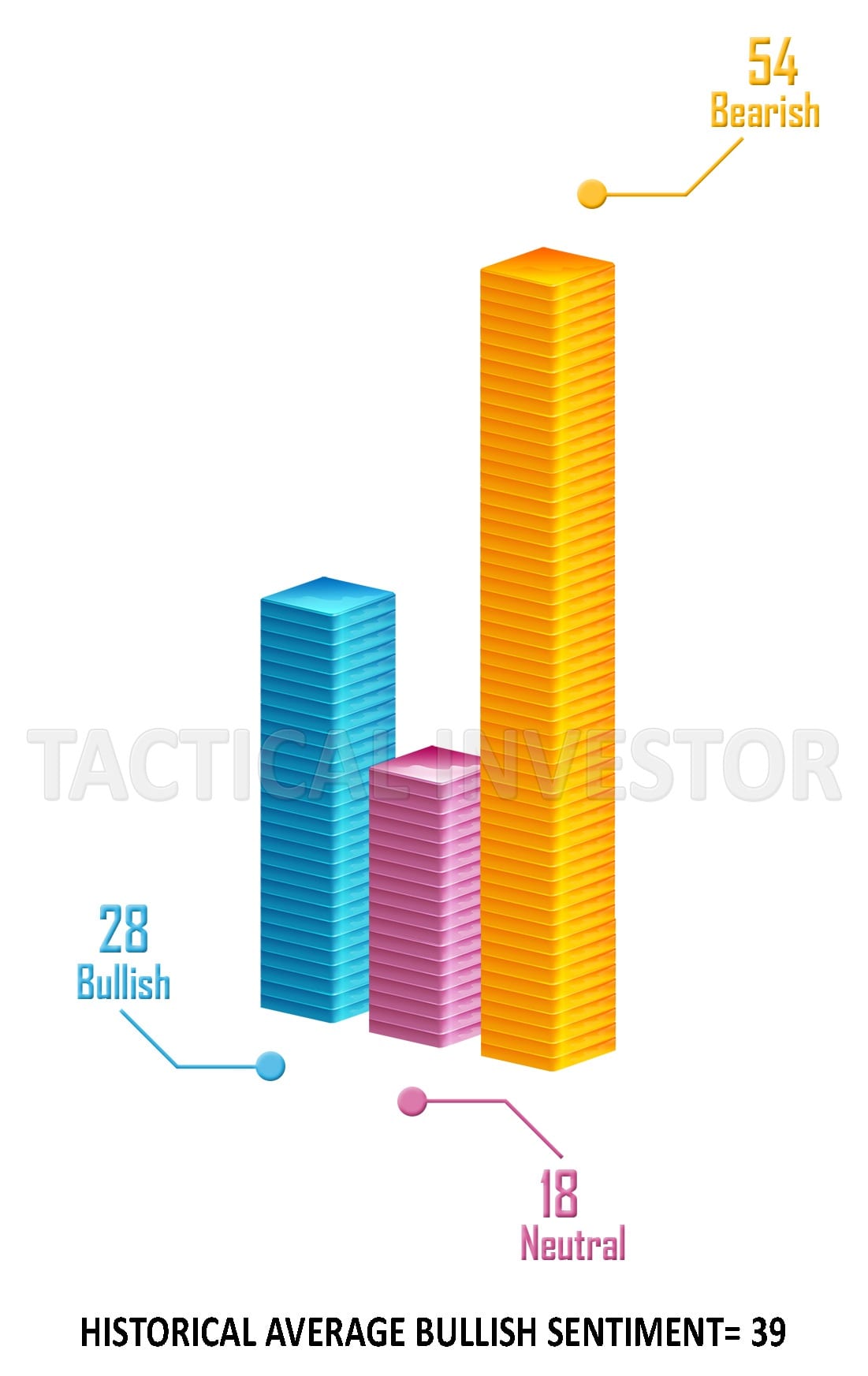

For the first time in approximately 24 months, bullish sentiment has surged to the 50% mark twice within a span of 6 weeks. Despite steadily climbing markets during this time, public sentiment has remained consistently negative. The current situation is distinct; while not reaching euphoria, the notable percentage change suggests a shift, indicating that a correction may be in the offing. Bonds are seeking support around the 148.00 range, and a weekly close below this level could lead to a test of the 142.00-144.00 ranges, with a possible overshoot to the 140 range. Fortunately, the downside risk for bonds appears limited.

The markets have displayed resilience against sharp corrections for an extended period, and a correction would be considered healthy for this market. Such an occurrence would instil fear among the masses, causing sentiment to turn negative again, thereby creating a foundation for the markets to rally higher.

The Mirage of Economic Recovery and the Fed’s Interest Rate Stance

The robust stock market paints a deceptive picture of a thriving economy driven by the influx of hot money. This illusion shatters if the supply of hot money diminishes, leading to a market downturn and dispelling the notion that everything is sound. If the economy were genuinely robust, the Fed would have raised interest rates more than just twice in the past decade. Yellen’s hedged statement, as presented at the beginning of this article, adds to the uncertainty.

Meanwhile, bullish sentiment has significantly surged on a percentage basis, and Bonds find themselves trading in the extremely oversold ranges. The conditions are ripe for a substantial correction. It’s crucial not to mistake this impending correction for a crash despite the pessimistic voices predicting doomsday scenarios. Our analysis relies on Mass Sentiment indicators and the Trend indicator. We’ll reconsider viewing significant pullbacks as buying opportunities once the trend turns negative.

Change of Heart, March 2020 Update

As we stated all along, the Current Fed Interest Rate stance was nothing but B.S. They lowered rates by 50 basis points and flooded the system with liquidity. All it took was a simple coronavirus attack to be blown out of proportion. The tactic worked as the masses panicked, allowing the Fed to push as much money into the system as they wanted without being questioned.

The Federal Reserve announced an emergency rate cut Tuesday of half a percentage point in response to the growing economic threat from the novel coronavirus. cnbc.com

They are also flooding the system with massive amounts of cash, as noted below:

The Federal Reserve today announced that it will launch a series of massive cash injections into funding markets and begin buying longer-term government bonds as panic over the coronavirus pandemic increasingly stresses the nation’s financial system.

The announcement that more than $1.5 trillion will be pumped into the banking system over the next two days comes as the Treasury market has shown signs of strain. Interest rates on U.S. government debt recently plunged to record lows as investors poured money into safe assets, but now trading in that market is not flowing smoothly. Politico

Stock market outlook March 12, 2020

This pullback has been so sharp that it’s virtually going to re-energize this bull, and Dow 39K could now become a possibility. Sounds insane. Well, that is precisely what our prediction for Dow 30K looked like when the Dow was trading below 21K, and it came to pass as the Dow came within striking zone of that target.

Our anxiety gauge has now dipped into the madness zone, something it has never done before, and if it remains here when our indicators pullback into the oversold ranges on the weekly chart, it could trigger the “father of all buy” signals.

As per our V-Indicator (the image on the top right of the market update), V readings have surged 650 points to an all-time new high of 8000. Its the most substantial one-week move, both in terms of percentage and points, since the inception of this indicator. The trend is positive, so when the markets reverse, the reversal will likely be solid and catch many players off guard.

Bearish Sentiment Surges: A Bullish Signal

An unmistakable shift has occurred as bearish sentiment has skyrocketed to a new 52-week high, potentially marking a multi-year peak. Equally noteworthy is the drop in Neutral sentiment, falling below 20, signifying a mass exodus from this camp, fueled by the belief that the bull market has met its end. While this may induce short-term anxiety, it’s excellent news for the long term, injecting several more years of vitality into this bull.

Adding to the positive outlook, bearish sentiment has also hit a multi-year high, painting another bullish picture. The most intriguing development is the anxiety index, which is currently trading in uncharted territory. If it sustains this level or deepens during periods when our weekly chart indicators are in the oversold to extremely oversold ranges, it could trigger a significant buy signal.

Drawing from historical patterns, it appears this bull market is not dead; it has taken a severe blow. Yet, looking back in 3 to 6 months, and especially 12-24 months, observers may be surprised and even shocked at the missed opportunity that slipped away during this moment of heightened bearish sentiment.

He that’s secure is not safe. Benjamin Franklin

Must-Read Articles Unveiled

Brain Control: Absolute Control Via Pleasure

Indoctrination: The Good, The Bad and the Ugly

Negative Thinking: How It Influences The Masses

Current Stock Market Trends: Embrace Strong Deviations

Stock Market Forecast For Next 3 Months: Up Or Down?

Stock Market Crash Date: If Only The Experts Knew When

Forever QE; the Program that never stops giving

What is Market Behavior? It’s Not the Question—It’s Time to Act

Brain Control: Domination via Pleasure

Power vs Force: Understanding Why Power Consistently Prevails

Benefits of Investing Early: Wealth and Serenity

9-5 Rat Race: Work Until You Die or Break Free?

Collective Euphoria: How Madness Fuels Financial Disaster

Strategic Ignorance: When Math Collides with Market Madness

Uptrend Stocks: Embracing the Renaissance of Market Prosperity

Overtrading: A Foolproof Recipe for Becoming a Burro in the Markets

Mob Psychology: Breaking Free to Achieve True Financial Success

What is the Bandwagon Effect? Exploring Its Impact

Hidden Positive Divergence: Harness Its Power to Dominate the Markets

Gold as Currency: A New Dawn?

Stock Market Correction History: Decoding Illusions Behind Crashes